China’s intended policy to ‘rebalance’ their economy with a greater focus on consumption rather than investment logically could have a negative impact on shipping, especially for large vessels that transport raw commodities to China such as capesize vessels. As more money is being spent domestically on consumer products and services, including either domestically procured or imported luxury goods, where there is more ‘value added quality’ than rudimentary processing of raw materials such as for real estate and infrastructure, big dry bulk vessels may be set for a tough few next years. A recent article in the New York Times on the ‘credit crunch’ and curtailing some of the ‘shadow banking’ may be an early precursor of what is to be expected.

The price of iron ore, the commodity with the highest seaborne trading volume after crude oil, over the last decade has increased threefold, primarily due to China’s insatiable demand due to urbanization and infrastructure-building spree. Iron ore with 62% ferrous content delivered to Tanjin has been quoted presently at about $130 per ton, a 20% improvement since May alone, when China embarked on a buying spree of the commodity in order to primarily replenish inventories.

Mining companies have been planning a $250 billion investment in order to expand capacity; most of the investment is planned by the industry’s major (and most bankable / competent) players, like Rio Tinto Group (RIO), Vale SA and BHP Billiton Ltd. (BHP), which implies a high degree of diligent execution and delivering of the projects on time. Given the lackluster world economic growth and China’s decelerating economy, most analysts expect a glut in the iron ore supply with prices set for a decline to levels around $100 per ton, on average, over the several years; some analysts even expect that temporarily iron ore may dip well below the $100 / ton mark, meaning rather bearish prospects for the commodity. As a general rule of thumb, bear commodity markets imply bear shipping markets, correspondingly, since there is a very high degree of correlation.

Just to re-ascertain the point of a bear iron ore market may not be good for the capesize vessels, most of the investments and the planned investments for increasing iron ore capacity are taking place in West Australia. In a recent report produced by Goldman Sachs, seaborne supply of iron ore is expected to grow from an estimate of about 1,150 mtpa in 2013 to approximately 1,500 mtpa in 2017, for an overall 30% increase. However, during the same interval, seaborne iron ore supply from Australia is expected to by 44% while from Brazil by ‘only’ 30%. Nothing shabby with these growth rates – as long as you are not a mining company, but, really not a cause to pop a champagne bottle for a shipowner.

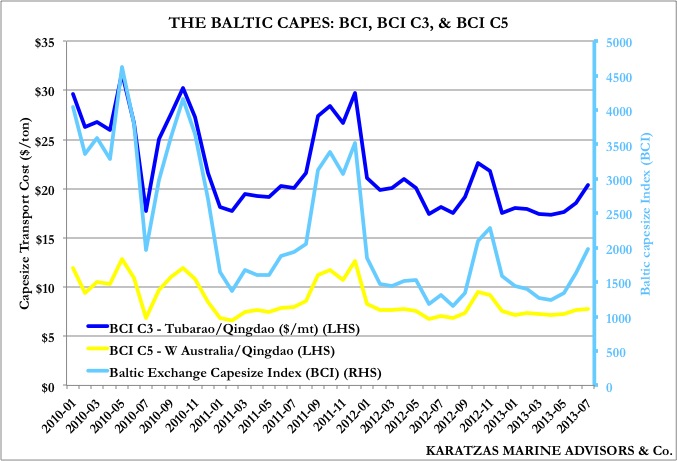

As anyone can quickly ascertain by taking a look at a world map, Australia is much closer to China than Brazil, and it takes three times more ships to transport the commodity from Brazil than from Australia to China. On August 16th, the Baltic Exchange in its daily report was posting the ‘C3 route’ Tubarao-Qingdao at $20.73/ton while the ‘C5 route’ W Australia-Qingdao at $9.01/ton.

{kind=link}

While over the next five years seaborne iron ore supply is expected to grow by 30%, the supply of capesize vessels (about 180,000 dwt) and Very Large Ore Carriers (VLOCs) (>200,000dwt) is expected to grow by 13% in the next three years, based on firmed, confirmed orders by bankable players (and thus high certainty of actual delivery of the vessels). This again is the firm, known supply, and with the shipbuilders with plenty of spare capacity and desperate need of new orders, it could easily be revised upwards. Not to mention that if iron ore gets cheaper, so it will be the case with newbuilding vessels, which could lead to another round of increased newbuilding frenzy. And, this, at a time when capesize vessels have been averaging $9,000 pd in the freight market, barely sufficient to cover their daily operating expenses (the less said the better on their financial cost, since some such vessels were bought for more than $100 million, and an ‘average’ term amortizing mortgage would presume more than $25,000 pd payment).

It has been said that you never appreciate a friend or ally until you are really in need. China in the last decade has been the cause of ‘irrational exuberance’ in shipping and its excesses thereof, and many other industries of course, such as the mining industry and their ‘commodities super-cycle’. Now that China seems to be slowing down, still to levels that many developed countries only would dream of, the ‘decoupling’ for many industries seems to be messier than expected. But again, China is full of surprises and broken projections …

© Basil M. Karatzas 2013 All Rights Reserved

No part of this blog may be reproduced, in whole or in part, under any circumstances, without the prior written consent of the copyright holder. Please contact: info@bmkaratzas.com

No comments:

Post a Comment