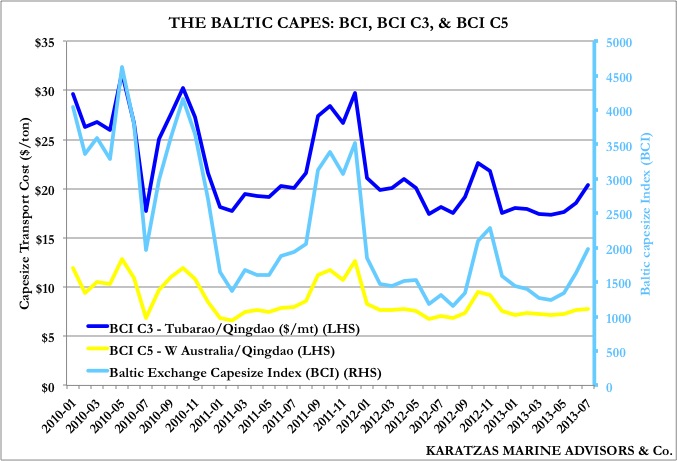

The Mystic Seaport museum in Connecticut launched in late July the sailing whaleship „Charles W Morgan”, allegedly the oldest and only remaining whaleship in the world. The „Morgan” was originally built in 1841 in New Bedford, Massachusetts when New Bedford and the adjacent area was then a major, and very prospering, whaling center worldwide. Like the wooden ships of her time, her expected life – between the dangers of limited maneuverability depending heavily on weather elements, cannibals and mutiny, Arctic ice and Confederate raiders, fire, woodworms, saltwater, was not expected to top twenty years, but it turned out that the „Morgan”, despite her many close calls, she ended up making an unheard of 37 voyages during eight decades of prime commercial life (average voyage duration was about four years.)

|

| Charles W Morgan - Outline |

It cost about $27,000 to built the vessel at the yard of Jethro and Zachariah Hillman, and about another $26,000 to outfit her, about $1.5 million in total in today’s money. Her least profitable trip made about $200,000 while her most profitable trip brought in about four million dollars, all at today’s purchasing power again. Over her trading career, she generated more than $32 million in gross profits (at today's PPP), mostly in the form of sperm oil, a waxy ester (prized as illuminant because of its bright, odorless flame), and whale oil made from the blubber of baleen whales (used for the production of soap, margarine and as cheaper illuminant due to her darker flame and fishy odor.) At 110 ft long, 27 ft beam and 17 ft draft, she had three decks, sailing capacity of 13,000 square feet and with about 35 crew, she was classed as a 351 ton whaling ship. She could hold 3,000 barrels of 31.5 gallons each; given that, on average, each whale could fill fifteen barrels, each of the voyages meant the life of 200 whales, implying that the ship has been the production plant (and graveyard) of 7,000 whales. Just one ship.

We are of the opinion that killing whales is a despicable practice in our days and ought to be banned altogether, but we have to admit that whaling was ‘big business’ a couple of centuries ago and the industry has been the cause for advancement of naval architecture and navigation, exploration and trade, and a pillar of the development and growth of most of the New England area in the USA and many other 'clusters' for the trade worldwide.

We feel strongly and enthusiastically about the Mystic’s diligent work to rebuilt and restore the vessel to her original condition based on tools and craftsmanship technique from the time of her original construction. The restoration so far has taken more than five years and has cost about seven million dollars employing 60 people.

|

| Charles W Morgan - preparing for launch day |

Imagine, if you please, what would be to sail on the vessel at her time: thirty five crew members packed in quarters no larger than two bedrooms, sailing around the Cape Horn for four years, away from families and loved ones, living on rations, no fresh food and vegetables onboard, with potable water stored in wooden casks for months, no bath, shower or toilet (just a ‘head’) battling the elements of nature, harpooning whales from the four small whale boats, towing the poor humongous beasts to the mother vessel, manually cutting, mincing, lifting, 'trying out' huge chunks of the meat, working on your knees and soaked in blood and fat (the decks of the vessel were not high enough to stand up, in order to preserve space.) With the exception of the captain and the first officer, a modern observer could justifiably say that being on the ship at such time was sort of voluntary indenture.

|

| Working Quarters - Detail view of elbows and frames supporting the weather deck |

How many things have changed since then? The ships; the people; the culture and the morals; ethics and what’s ‘right’ and ‘wrong’; major trades and industries important to local societies and even nations… Ships always have a story to share… from the people who dreamt of them, to the people who built them, to the people who sailed on them, to the people who serviced them, to the people who restored them way past their trading life ... we should take a minute listen to their sort of 'Siren song'!

|

| Charles W Morgan - Past Glory (Photo credit: Mystic Seaport) |

© 2013 Basil M Karatzas & Karatzas Marine Advisors & Co.

Unless otherwise stated, images are provided by Karatzas Marine Advisors & Co. No part of this blog can be reproduced by any means or under any circumstances, in whole or in part, without proper attribution or the consent of the copyright and trademark holders.

{kind=link}